Article Review: Tougher than IRS? California Franchise Tax Board

California residents and business owners in the state who are audited by IRS have a responsibility to report their IRS audit findings to the California Franchise Tax Board. While IRS will send the results of your audit to the state agency, it is in your best interest to self-report the results of your audit and prevent the possibility of a CTFB review of your federal audit results.

Typically, Internal Revenue Service (IRS) audits back three years, but that time frame can be extended under various circumstances. In California specifically, IRS has an unlimited time frame to audit records if:

- You never filed taxes.

- Tax forms are found.

- Tax forms are found incorrect.

Simply put, if IRS wants to extend an audit timeframe, they can and will find a way to extend the audit time period.

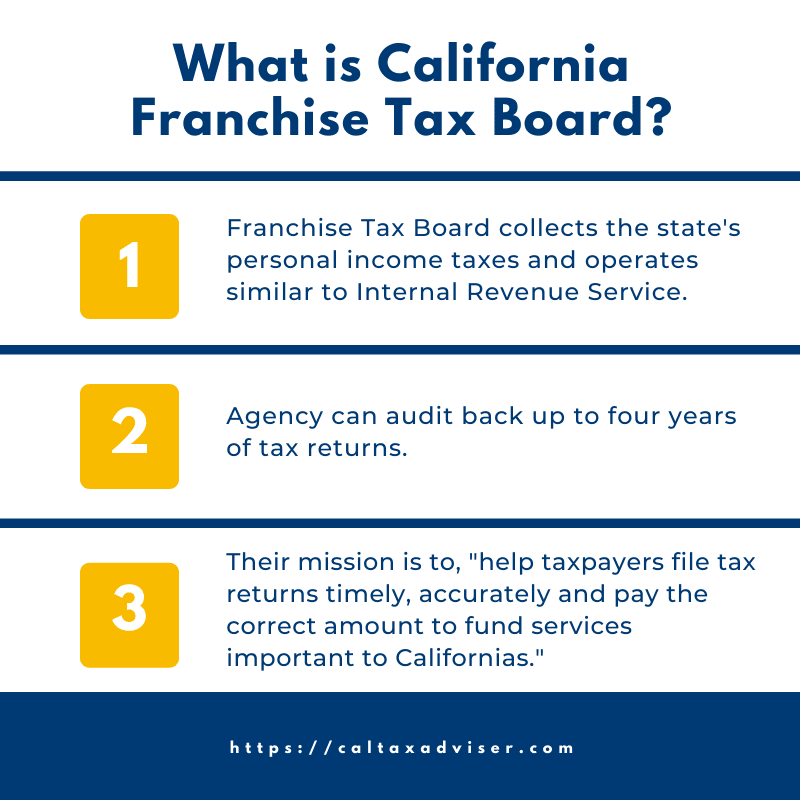

What is the role of the California Franchise Tax Board?

Franchise Tax Board (FTB) collects the state’s personal income taxes and can audit back four years of tax returns. According to the FTB, their mission is to, “help taxpayers file tax returns timely, accurately, and pay the correct amount to fund services important to Californians.”

If an IRS audit assessment concludes with findings of an underpayment, there’s more to be done for the audited party than simply agreeing and paying fines. After an audit, CA Franchise Tax Board (FTB) must be notified of the claims within six months. If the agency is not notified, they will find out, it’s just a matter of time. It could take a couple of years for FTB to find they were not notified of IRS audit findings.

While IRS will report audit findings to FTB, the agency is severely backlogged and often does not report the results of an audit within the 6 month window. It is in a business owner’s interest to self report because the state agency will re-open the audit to ensure that they were not shorted in the audit collection. By reporting your audit findings you can save yourself time and effort of another review of your tax filings.

Failure to notify FTB within the six-month time frame does not terminate the California Statute of Limitations. This means FTB no longer has a limited time frame to initiate legal proceedings to investigate your case. Legally, FTB can send tax bills to your business 4 or more years later if they are not notified within the six-month window.

CA FTB can return years later to examine income assessed during the past IRS audit, and carry it over as money owed to the State of California. Notifying FTB within the six-month window of an IRS audit closure ensures you don’t waive any potential rights you have to petition or fight that assessment.

The benefits of notifying FTB of IRS audit closures are:

- Even if you do lose with the IRS you potentially could provide documents and work through those issues with the FTB.

- Penalties and interest accrue over time. Assessing if you really think you owe early on helps avoid further costs.

Best practice during audits is to find a certified tax attorney to represent you. If either you or your attorney receives notice from FTB within six months, or even if you don’t hear from FTB, you can file an amended return or notify the agency and file a petition to dispute results during IRS audit findings.

If FTB requests an audit extension, agreeing to the requested extension looks better and gives them less reason to think there is fraudulent or suspicious activity. Denying an extension of time request can actually raise suspicion or trigger assumptions even if there isn’t any suspicious activity occurring.

FTB and IRS audits are conducted in a very similar way. After audit findings, you can dispute results with the California Office of Tax Appeals (OTA). Appealing with FTB themselves is more difficult.

Learn more about California Franchise Tax Board in the full Forbes article below.

Article Review: Tougher than IRS? California Franchise Tax Board

“When it comes to taxes, most people think about the IRS. But if you live or do business in California, state taxes are a big piece of what you pay. California does a good job of aggressively drawing people into its tax net of high individual (13.3 percent) and business (8.84 percent) tax rates. Add the state’s notoriously aggressive enforcement and collection activities, and it’s a perfect storm.

The state’s tax system is complex too. Rather than adopting federal tax law wholesale like many states, California’s legislators pick and choose. California adopts some federal rules but not others, so its tax law has many nuances that do not track federal tax law. Even California’s tax agencies and tax dispute resolution system are unusual. Combined with its unique tax statute of limitations, the situation can be downright scary.

Take California’s long tax audit period. The basic IRS statute of limitations is three years. In some cases, the IRS gets six years, not three. But barring those kinds of exceptions, the IRS usually has three years once you file a return to audit. The California Franchise Tax Board administers California’s income tax.

The FTB gets an extra year, so it has four years, not three. That sounds simple, just an extra year, but not so fast. Say that you are involved in an IRS audit, but the IRS has not yet issued a notice of deficiency (also called a 90-day letter, which must come via certified mail).

You may want to drag your feet in the IRS audit, to try to put you outside California’s four-year reach. Hey, with a little delay, maybe you can outrun California’s four-year statute, you might think. Will that protect you from California’s follow-along ‘‘me, too’’ request for money?

Unfortunately, no matter how long your IRS dispute goes on, California can always piggyback and collect its share. Several things can give the FTB an unlimited amount of time. California, like the IRS, gets unlimited time to come after you if you never file an income tax return.

The same goes for false or fraudulent returns. Those are obvious, but there are other dangers, too. In some other, less intuitive cases, California also gets unlimited time to audit.

Suppose that an IRS audit changes your tax liability. Perhaps you lose your IRS case, or you just agree with the IRS during an audit that you owe a few more dollars. You might simply sign and send back a form to the IRS. In that event, you are obligated to notify the California FTB within six months.

If you fail to notify the FTB of the IRS change to your tax liability, the California statute of limitations never runs. That means you might get a tax bill 10 or more years later.

Yes, it happens. California’s FTB often comes along promptly after the IRS to ask for its piece of a deficiency. But regardless of whether California gets notice of the adjustment from the IRS, California taxpayers must notify the FTB and pay up. If you forget, they usually find you at some point. This coattails concept in California law applies to amended tax returns as well.

If you amend your IRS tax return, California law requires you to amend your California return within six months if the change increases the amount of tax due. If you don’t, the California statute of limitations never expires.

With all of those rules, should you ever voluntarily give the FTB more time to audit you? Surprisingly, yes. Again, the basic rule is that the FTB must examine your tax return within four years of when you file.

But like the IRS, the FTB sometimes will contact you, asking for more time. The FTB may send a form, asking you to sign it to extend the period of limitations. This part of California’s system operates pretty much like its federal counterpart.

Some taxpayers just say no, likening an extension to allow the government more time to audit to giving a thief more time to burglarize your home. But with the IRS or FTB, saying “no” usually triggers an assessment, generally based on adverse assumptions. So, you should usually agree to the extension, which you may be able to limit to specified tax issues, or to limit the added time.

How about California audits and tax disputes? They tend to be harder to resolve than IRS ones, on average. There are lots of taxes too. California has income taxes, franchise taxes, sales and use taxes, property taxes, and excise taxes. There are nexus issues, withholding taxes, tough residency rules, and more. If you have an IRS dispute, you can fight it administratively with the auditor and at the IRS Appeals Office.

If necessary, you can go to U.S. Tax Court, where you can contest the taxes before paying before a judge who decides only tax cases. Alternatively, if you are willing to pay the tax first, you could proceed to the U.S. Court of Federal Claims, or U.S. District Court. Many states have a state tax court, but California does not. For decades, it had the State Board of Equalization (SBE), a five-member administrative body—the only elected tax commission in the U.S.—that functioned much like a court.

It was a quirky and controversial system. But all of that changed in 2017 when California legislators enacted the Taxpayer Transparency and Fairness Act of 2017, which created the California Office of Tax Appeals (OTA). The OTA has jurisdiction for appeals related to taxes administered by the California Department of Tax and Fee Administration (CDTFA) and the Franchise Tax Board (FTB). That includes personal income taxes, corporate franchise taxes, sales and use taxes, LLC taxes and fees, even gas tax and other excise taxes.

But before you get to the OTA, you’ll be dealing with California’s tax agencies, either the CDTFA or the FTB. Both have audit processes, and both have administrative processes that allow taxpayers to resolve differences over the proper assessment of tax and the imposition of any penalties. If your audit is with the Franchise Tax Board over your income taxes, the process isn’t too different from federal. The auditor will eventually write up what he or she thinks, and most likely will propose some additional taxes.

If you disagree, you should write to the FTB and go through the FTB’s appeals process. But compared to the IRS Appeals Office, the FTB’s appeals process does not seem to resolve too many cases, so you may end up having to go to the OTA. The FTB also has programs that allow settlement, offers in compromise, and payment plans.

However, once again, those generally do not work as well as their IRS counterparts. In the event a dispute persists after the CDTFA or FTB make a final tax determination, you can appeal to the Office of Tax Appeals.

The OTA is an independent office that is separate from the state’s tax agencies. The OTA is dedicated solely to the adjudication of California tax disputes. An appeal to OTA presents the final opportunity for taxpayers to resolve their tax disputes with the state’s tax agencies administratively, without going to court.

Appeals may be made by a letter request to OTA, accompanied by any supporting documents. You can ask for an oral hearing, which is usually a good idea. You can even bring witnesses who can testify before the OTA.

Prior to the hearing, taxpayers should provide all relevant documents to OTA and may ask, or be asked, to participate in a pre-hearing conference. Each tax appeal is heard by a panel of three administrative law judges (ALJs), each of whom has significant experience with tax law.

One ALJ will be designated as the lead ALJ for the purposes of the hearing, but every panel member will participate equally in the hearing, deliberations and decision. Generally, the ALJ panel will prepare a written decision within 100 days of the hearing, along with information about further steps that may be taken if the taxpayer disagrees with the OTA’s decision.

If you do not agree with OTA’s decision on a case involving a tax assessment, you can pay the tax liability and then file a claim for refund with the FTB. If the FTB denies your claim, you can file an action against the FTB in California Superior Court within 90 days of the denial of your claim for refund.

If you do not agree with OTA’s decision on a case involving a denial of a claim for refund, you can file an action against the taxing agency in California Superior Court within 90 days of OTA’s decision becoming final. All actions filed in Superior Court are reviewed de novo by the court, rather than being based on the OTA decision. Cases coming out of the CDTFA follow the same procedure.”

Learn more

Have you received an audit letter from CA FTB or IRS? Learn more about what your audit response letter should include, tips to navigate a response letter, and what you should and shouldn’t do in this article, “How to Respond to IRS Letter 6323.”